The Real Asset Spilt of Financially Independent Canadians

Today I want to talk about something that doesn’t get discussed enough when it comes to financial independence. Especially here in Ontario.

And that’s this: How much of your net worth should actually be tied up in your home versus your investments?

In Canada, we’ve been conditioned to believe, “Your house is your investment.”

Is it really helping you become financially independent, or is it quietly slowing you down?

Let’s break it down.

The Mindset Problem

If you live in the Greater Toronto Area (GTA), you know how this goes. You talk to a mortgage broker or go to a bank, you get approved for a certain amount, and most not all, buy right up to the limit they got approved for

The most common sayings when buying a home is: Real state always goes up. This is a good investment

But here’s the reality that no one tells you: Your primary residence does NOT produce income.

It doesn’t pay you monthly.

It doesn’t fund your retirement.

Unless you downsize or sell, it’s just equity sitting there.

When you maximize the amount of debt to purchase a home, can you really afford it?

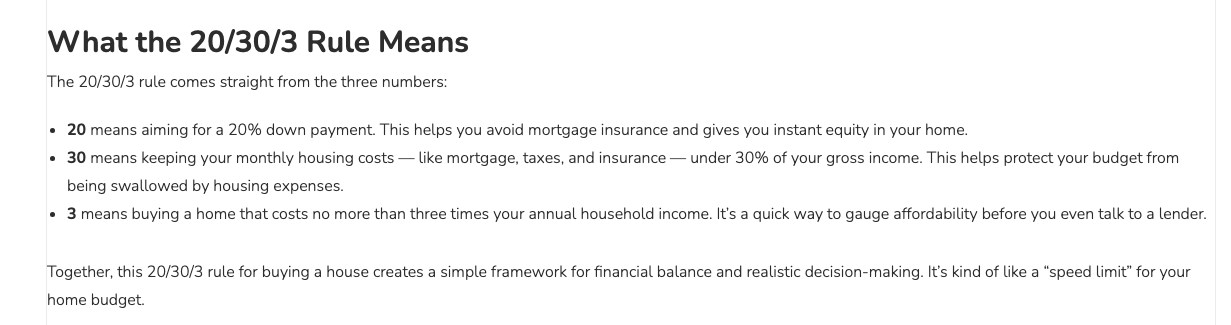

Are you breaking the 20/30/3 rule to purchase the home to avoid being house poor ?

The rules states you should have a 20% downpayment, only have 30% of your income a month go towards housing and the total purchase price of the home, should be more no more than 3 times your annual household income.

If you don’t follow those rules, your left with a heavy mortgage payment with less money at the end of the month to invest.

What Financially Independent People Actually Do

When you look at people in Ontario who are actually pursuing or have achieved financial independence, they have a different asset allocation.

A typical breakdown might look like:

50–70% in investments

ETFs

Stocks

Rental properties (cash flowing)

Retirement accounts (R in RSP, TFSA)

20–40% in their primary residence

5–10% cash or liquid reserves

The key difference is they don’t overextend on their home. Just because they can afford a $1M house, doesn’t mean they buy it.

They might choose:

A smaller home

A townhouse instead of detached

Or even continue renting

Why? Because they understand one simple principle: Cash flow builds freedom. Not equity alone.

It’s funny because just the other day, I was talking to a guy in the gym, and he’s a big real estate guy and always talks about how he built his portfolio of homes that all cash flow.

The Big House Trap

This was an important thing for me as I purchased a home with my wife last year.

We didn’t want to take the max that we could borrow, have a large mortgage and have minimal investments.

We wanted an affordable house, a lower mortgage and a surplus at the end of the month to focus on investing.

I don’t want to grow older and have more home equity and a limited investment portfolio cause most on my income is going towards a mortgage.

I want a strong investment portfolio, passive income building with options, flexibility and freedom

I believe the people chasing the big house vs people chasing being financially independent, is that one is optimizing for the lifestyle today, while the other is optimized for freedom tomorrow.

Homeownership vs Financial Independence

According the stats Canada, In Ontario about 68% of people own a home, So that means roughly, 2 out every 3 people own a home.

There is no official stat for people who are financially independent, but lets look at some wealth numbers.

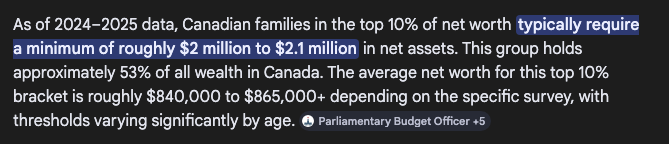

To be in the top 10% of wealth in Canada, have to have a net worth of 1.5-$2M.

The top %1, is over 8M.

Most people who have achieved f.i.r.e. Have about $1M-2.5M invested

Some people have over a 1M net worth just in their home, but are not financially independent.

So realistically, it maybe less them 10% of people. Maybe even closet to 5%.

So that means, 68% of people in Ontario own a home, but only 5-10% are financially independent.

Why Some Financially Independent People Even Rent

Some financially independent individuals in Ontario actually choose to rent. It’s not because they can’t buy, It’s because they run the numbers.

They look at:

Cost of ownership vs renting

Opportunity cost of tying up capital

Flexibility

To even go further on this myself to get a better understanding, I just ordered a book titled “Quit like a Millionaire” from Toronto couple Kristy and Bryce

They are couple that reached financial independence in their early 30’s, from Toronto, without purchasing a home.

Just listened to a podcast they were on the other day.

The Balance I’m Aiming For

As I stated before, there are people who have achieved financial independence without buying a home, however that was something important for me and my wife.

We were both raised in a home and want that for our future family.

So far so good as we purchased something using the 20/30/3 rule.

Right now it’s about, keeping expenses manageable, growing income and a heavy focus on investments.

The investments are what will:

Pay you in retirement

Give you options

Create real financial freedom

1.2-1.5 million in investments I believe would the sweet spot